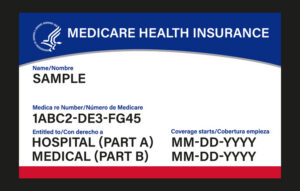

Medicare can feel confusing at first, but understanding the basics can help you make more informed healthcare and financial decisions as you approach retirement. Medicare is generally broken into four parts — A, B, C, and D — each covering different healthcare needs.

Part A primarily covers hospital care and is typically free for individuals who have worked and paid into Medicare for at least 10 years. Part B covers doctors, outpatient care, and approximately 80% of medical costs. However, Part B comes with a monthly premium that is income-based and can increase significantly for higher-income retirees. Because Part B only covers about 80% of approved expenses, many individuals choose to add a supplemental plan, such as a Medicare Supplement Plan G, to help cover the remaining costs. Usually, the best time to enroll in a supplemental plan is during the 6-month Medigap Open Enrollment period. It starts the first month you have Medicare Part B. Prescription drug coverage is generally handled through Part D plans, which vary based on medications and coverage needs.

One important detail many people overlook is that Medicare premiums can rise substantially depending on income during retirement. Financial professionals often recommend diversifying retirement savings across different account types to help better manage future taxable income and healthcare costs. As with any important financial or healthcare decision, reviewing your options carefully and speaking with trusted professionals can help you select the coverage that best fits your needs.